Medicare is the federal health insurance program for:

People who are 65 or older

Certain younger people with disabilities

People with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a transplant, sometimes called ESRD)

What are the parts of Medicare?

The different parts of Medicare help cover specific services:

Medicare Part A (Hospital Insurance) Part A covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care.

Medicare Part B (Medical Insurance) Part B covers certain doctors’ services, outpatient care, medical supplies, and preventive services.

Medicare Part D (prescription drug coverage) Helps cover the cost of prescription drugs (including many recommended shots or vaccines).

Part A & Part B Premiums

Most people don’t pay a monthly premium for Part A.

You usually don’t pay a monthly premium for Part A if you or your spouse paid Medicare taxes while working for a certain amount of time. This is sometimes called “premium-free Part A.”

If you don’t qualify for premium-free Part A, you can buy Part A.

If you aren’t eligible for premium-free Part A, you may be able to buy Part A. You’ll pay up to $506 each month in 2023. If you paid Medicare taxes for less than 30 quarters, the standard Part A premium is $506. If you paid Medicare taxes for 30–39 quarters, the standard Part A premium is $278.

Most people will pay the standard Part B premium amount. The standard Part B premium amount in 2023 is $164.90. If your modified adjusted gross income as reported on your IRS tax return from 2 years ago is above a certain amount, you’ll pay the standard premium amount and an Income Related Monthly Adjustment Amount (IRMAA). IRMAA is an extra charge added to your premium.

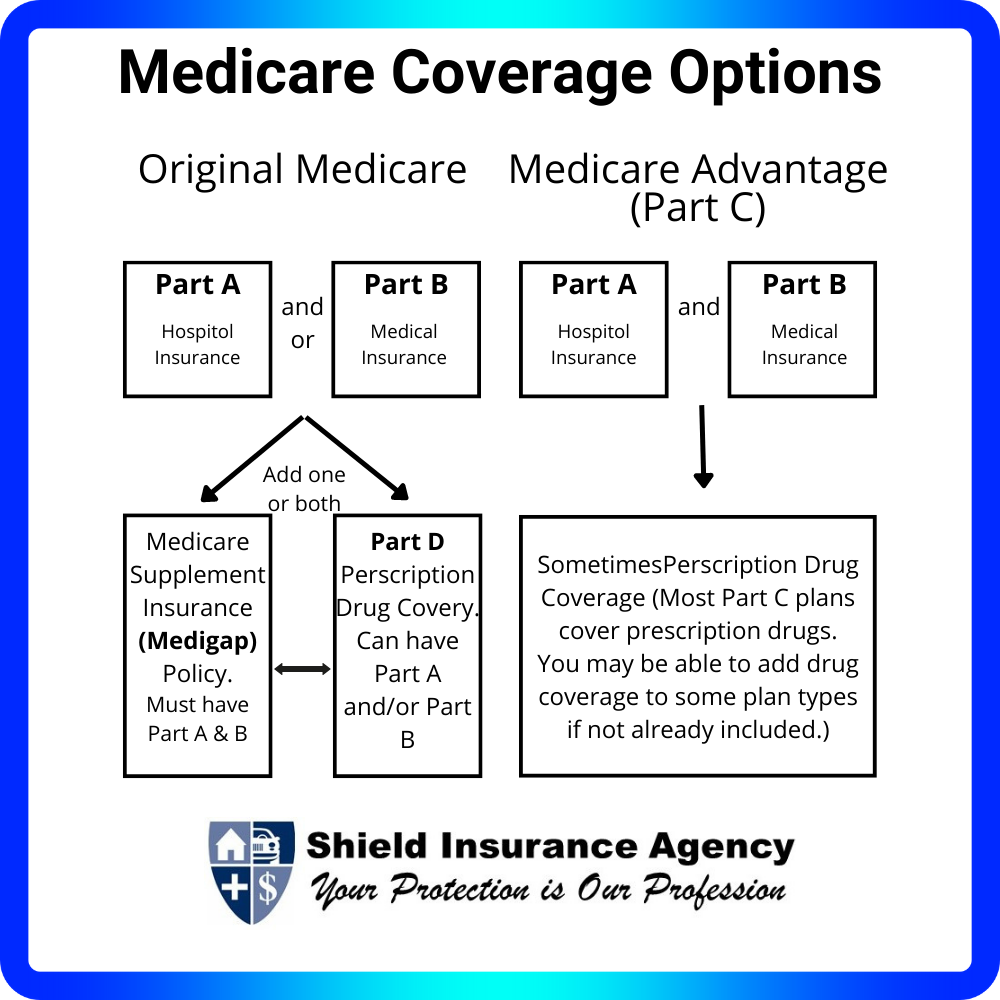

Original Medicare includes Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance). You pay for services as you get them. When you get services, you’ll pay a deductible at the start of each year, and you usually pay 20% of the cost of the Medicare-approved service, called coinsurance. If you want drug coverage, you can add a separate drug plan (Part D).

Original Medicare pays for much, but not all, of the cost for covered health care services and supplies. A Medicare Supplement Insurance (Medigap) policy can help pay some of the remaining health care costs, like copayments, coinsurance, and deductibles. Some Medigap policies also cover services that Original Medicare doesn’t cover, like emergency medical care when you travel outside the U.S.

Medicare Advantage is Medicare-approved plan from a private company that offers an alternative to Original Medicare for your health and drug coverage. These “bundled” plans include Part A, Part B, and usually Part D. Plans may offer some extra benefits that Original Medicare doesn’t cover — like vision, hearing, and dental services. Medicare Advantage Plans have yearly contracts with Medicare and must follow Medicare’s coverage rules. The plan must notify you about any changes before the start of the next enrollment year.

In October 2020, the federal government issued the “transparency in coverage” final rule under the Federal No Surprises Act. The rule provides protection against balance or “surprise” billing under certain circumstances, and phases in new transparency requirements on most group health plans and health insurers. The purpose of the requirements is to enable consumers to make informed healthcare purchasing decisions.

What is “balance billing” (sometimes called “billing surprises”)?

When you see a doctor or other health care provider, you may owe certain out-of-pocket costs, such as a copayment, coinsurance, and/or a deductible. You may have other costs or have to pay the entire bill if you see a provider or visit a healthcare facility that isn’t in your health plan’s network.

Nonparticipating describes providers and facilities that haven’t signed a contract with your health plan. Nonparticipating providers may be permitted to bill you for the difference between what your plan agreed to pay and the full amount charged for a service. This is called balance billing. This amount is likely more than in-network costs for the same service and might not count toward your annual out-of-pocket limit.

Surprise billing is an unexpected balance bill. This can happen when you can’t control who is involved in your care, such as when you have an emergency or schedule a visit at a participating facility but are unexpectedly treated by a nonparticipating provider.

Your rights and protections against Surprises

When you get emergency care or get treated by a nonparticipating provider at a participating hospital or ambulatory surgical center, you are protected from balance or surprise billing. Services you are protected from balance billing for:

Emergency services

If you have an emergency medical condition and get emergency services from a nonparticipating provider or facility, the most the provider or facility may bill you is your plan’s in-network out-of-pocket amount, such as copays, coinsurance, and deductibles. You can’t be balance billed for these emergency services. This includes services you may get after you’re in stable condition unless you give written consent and give up your protections not to be balanced billed for these post-stabilization services.

Michigan law also protects you from balance billing and requires that you pay only your in-network cost-sharing amounts for (i) covered emergency services provided by an out-of-network provider at an in-network facility or out-of-network facility; (ii) covered nonemergency services provided by an out-of-network provider at an in-network facility if you do not have the ability or opportunity to choose an in-network provider; and (iii) any healthcare services you receive at an in-network facility from an out-of-network provider within 72 hours of receiving services from that facility’s emergency room.

Certain services at a participating hospital or ambulatory surgical center

Medical Insurance is a crucial aspect of our lives that we often overlook until we need it. It provides us with financial protection against unexpected medical expenses, which can be quite expensive. Health insurance covers a wide range of medical services, including doctor visits, hospitalization, surgeries, and prescription drugs. In this blog post, we will discuss the benefits of health insurance and why it is essential to have.

One of the most significant benefits of medical health insurance is that it helps you manage your medical expenses. With health insurance, you pay a monthly premium, and in return, your insurance company covers a portion of your medical expenses. This means that you don’t have to worry about paying the full cost of medical services out of your pocket. However, it is important to note that most health insurance plans have a deductible, which is the amount you have to pay before your insurance coverage kicks in. Once you reach your deductible, your insurance company will cover a portion of your medical expenses.

Another benefit of medical insurance is that it covers prescription drugs. Prescription drugs can be quite expensive, especially if you need to take them regularly. With health insurance, you can get your prescription drugs at a lower cost, which can save you a lot of money in the long run. Some health insurance plans also cover preventive care, such as annual check-ups and screenings, which can help you detect health problems early on.

Health insurance also promotes well-being, both physical and emotional. With health insurance, you have access to medical services that can help you maintain your physical fitness and overall health. This includes regular check-ups, screenings, and access to specialists if needed. Additionally, some health insurance plans offer wellness programs that focus on nutrition and wellness, which can help you maintain a healthy lifestyle.

Emotional Health is part of Medical Insurance

Emotional health is also an important aspect of well-being, and health insurance can help you manage your mental health. Mental health services, such as therapy and counseling, can be quite expensive without insurance. With health insurance, you can get the help you need without worrying about the cost. This can be especially important for those who struggle with mental health issues, such as anxiety and depression.

Health insurance also benefits families. With a family health insurance plan, you can cover your entire family under one policy. This means that you don’t have to worry about getting individual policies for each family member. Additionally, family health insurance plans often offer lower premiums than individual plans, which can save you money in the long run.

In conclusion, health insurance is essential for managing medical expenses and promoting well-being. It covers a wide range of medical services, including doctor visits, hospitalization, surgeries, and prescription drugs. Health insurance also promotes physical and emotional health, as well as nutrition and wellness. Additionally, it benefits families by providing coverage for the entire family under one policy. If you are looking for health insurance, contact Shield Insurance Agency for all of your insurance needs at (616) 896-4600.

Health insurance is a crucial aspect of our lives that we often overlook until we need it. It provides us with financial protection against unexpected medical expenses that can arise from sickness, injury, or any other medical condition. In this blog post, we will discuss the benefits of health insurance and why it is essential to have it.

Health Insurance Bills

One of the most significant benefits of health insurance is that it helps you manage your medical bills. Medical bills can be expensive, and without insurance, you may find yourself struggling to pay them. Health insurance covers a portion of your medical expenses, which can help you save a significant amount of money. The amount of coverage you receive depends on your policy, but it can cover anything from doctor visits to hospital stays.

Another benefit of health insurance is that it helps you manage your deductibles. A deductible is the amount of money you pay out of pocket before your insurance coverage kicks in. With health insurance, you can choose a deductible that fits your budget and needs. This means that you can choose a higher deductible to lower your monthly premiums or a lower deductible to pay less out of pocket when you need medical care.

Prescriptions are another area where health insurance can be beneficial. Prescription drugs can be expensive, and without insurance, you may find yourself struggling to afford them. Health insurance can help cover the cost of prescription drugs, which can make it easier for you to manage your medical condition.

Injury and sickness are two of the most common reasons people need medical care. Health insurance can help cover the cost of medical care for both injuries and sickness. This means that you can get the medical care you need without worrying about the cost.

Medical emergencies can happen at any time, and they can be expensive. Health insurance can help cover the cost of emergency medical care, which can be a lifesaver in a medical emergency. This means that you can get the medical care you need without worrying about the cost.

Finally, health insurance can be beneficial for your family. If you have a family, you want to make sure that they are protected in case of a medical emergency. Health insurance can help cover the cost of medical care for your family, which can give you peace of mind.

In conclusion, health insurance is essential for anyone who wants to protect themselves and their family from unexpected medical expenses. It can help you manage your medical bills, deductibles, prescriptions, and emergency medical care. It can also be beneficial for your family. If you are looking for health insurance, contact Shield Insurance Agency for all of your insurance needs at (616) 896-4600. They can help you find the right policy for your needs and budget.

Christian Bowers has Down Syndrome but likes to do normal guy stuff like go bowling and play video games.

Making friends was never hard for the young man, now 24, until he finished school and found, as many people without Down Syndrome do for that matter, it’s not as easy and straightforward to maintain a social life.

Bowers’ mother, Donna Herter, watched her son sink further and further into the dumps because he didn’t have any friends to visit him.

Eventually, Herter put up a post on Facebook asking if any local guys near Rochester, Minnesota, would be interested in coming to hang out with Christian for two hours, a service for which she was willing to offer $80,00 in compensation.

A nurse on the night shift put the post up at 4:00 AM before ending her workday and going to sleep. When she woke up, it had amassed 5,000 comments.

“I was freaking out. My hands were shaking, I was sweating. I was just looking for some local guys, I didn’t want to invite like the entire world into our house,” she told CBS News.

Her friends encouraged her to calm down and take a closer look at the comments, in which she found parents offering suggestions and others volunteering to help.

She eventually found 7 fellows from Wentzville, Minnesota, who visit Christian once a week on a rotating schedule. Herter says her son goes to sleep with a smile on his face now, and is excited about life in general, and of the future as well.

Friendships are important for people born with Down Syndrome, and associations urge parents to plan for the eventuality of their child exiting school and needing to take a more precise attitude towards socializing.

Christian occasionally attends gatherings and groups of other special needs men and women his age, but craves friendship with the rest of the population as well.

“And I’ve never asked him, but I assume because it kind of makes him feel normal, just for an hour or two. ‘Hey, somebody who doesn’t have Down syndrome wants to hang out with me,’” she said.

One of the 7 friends, James Hasting, said he felt terrible that Herter had reached the point where she was trying to pay people to visit her son. Hasting, who volunteers with special needs folks, said hanging out just for a few hours to watch a movie or play video games with Christian has changed the way he looks at the world.

Many people don’t realize that Medicare decisions can have financial implications, and Medicare costs can be incorporated into comprehensive financial planning.

“When and how can I enroll in Medicare?” “How much does Medicare cost and what does it cover?” are all common questions you may have regarding your health care plan for retirement.

In addition to working closely with your financial planner, you can assess specific Medicare drug and health care plan costs by utilizing online tools.

Every day, around 10,000 members of the Baby Boomer Generation turn age 65, which is generally the age they become eligible for Medicare. [1][2] Often, this is the first time that many Baby Boomers realize that decisions around Medicare aren’t just medical decisions; Medicare decisions also have significant financial implications. Once you come to this realization, you can turn to the financial professionals on whom you depend to help make sense of Medicare and in turn help you make financially sound Medicare decisions.

Understanding Medicare can be difficult, but the Nationwide Retirement Institute® is here to help you by sharing some of the most common Medicare questions. Working with a financial professional and utilizing various planning tools can help you incorporate Medicare costs into your financial plan.

When do I enroll in Medicare?

For everyone who turns 65 and is eligible for Medicare, there’s a seven-month “initial enrollment period,” or IEP. The IEP spans from the start of the third month before your 65th birthday through the end of the third month following the month of your 65th birthday. This IEP is available regardless of whether you continue to work past age 65.

If you choose to work past age 65 and remain eligible for group health coverage provided by your employer (or your spouse’s employer), then you may choose not to enroll in Medicare during your IEP. If this is the case, you’ll have a second chance to enroll during a “special enrollment period,” or SEP. The SEP generally lasts 8 months, beginning from the month after your employment or group health coverage ends, whichever occurs first. If you do not enroll in Medicare during your IEP or SEP, then you must wait to sign up during the General Enrollment Period between January 1st and March 31st of each year; but beware that in this circumstance, you may be subject to lifelong penalties in the form of increased premiums once you do enroll.

How do I enroll in Medicare?

That depends.

If you are already receiving Social Security when you turn 65, you will automatically be enrolled in Original Medicare, which means Medicare Parts A & B. Your eligibility will be effective the first day of the month you turn 65. You will not even need to sign up. You should simply receive a red, white, and blue Medicare card in the mail around three months before your 65th birthday.

If you choose to stay on Original Medicare, you will likely want to proactively enroll in a Medicare Part D plan as well, to get prescription drug coverage. In the alternative, you may choose to enroll in a Medicare Advantage Plan, which is known as Medicare Part C. Medicare Advantage plans to replace Original Medicare and Medicare Part D, but you must proactively enroll in Medicare Advantage plans as well. You can enroll in a Medicare Advantage Plan or a Medicare Part D plan during your IEP.

Medicare.gov/plan-compare shows specific Medicare drug plans and Medicare Advantage plan costs, and you have the opportunity to call the plans you’re interested in to get more details. For help comparing plan costs, the State Health Insurance Assistance Program (SHIP) can also assist you.

If you’re not already receiving Social Security at least 4 months before turning 65, you’ll need to sign up by:

Applying online at Social Security. (If you start your online application and receive a re-entry number, you can go back to Social Security to finish your application at a later time.);

Visit their local Social Security office; or

Call Social Security at 1-800-772-1213 (TTY: 1-800-325-0778).

Nationwide teamed up with the National Council on Aging (NCOA) to create an unbiased tool to help sort through Medicare options. It’s called the NCOA My Medicare Matters® tool brought to you by Nationwide. The tool allows you to work with financial professionals so that they can assist you in the Medicare decision-making process before the completion of the enrollment process.

How much does Medicare cost?

That also depends. The first and most important thing to understand in the context of cost is that it will not be free! There are still premiums, copays, coinsurance, and deductibles to plan for.

If you sign up for Original Medicare, Part A will be free if you have paid at least 10 years of Medicare taxes. Part B will require a monthly premium of $170.10 in 2022. [3] That amount may be more if your income is high enough to cross certain thresholds.

Medicare Part D (for prescription drugs) and Medicare Advantage plans (Part C, an alternative to Original Medicare and Medicare Part D) will also have monthly premiums. The costs of those premiums will vary plan by plan and be impacted by other factors, like your age at enrollment and geographic location.

What does Medicare cover?

Not everything! That may be the simplest yet most important fact you need to understand. Medicare will not cover all medical care.

In particular, Medicare does not cover long-term care (LTC), nor vision or dental care. Also, Medicare does not cover care received outside of the USA. This means that supplemental insurance for LTC, dental and vision, and travel insurance, will be important to look into.

That being said, Medicare does cover most medical treatments and procedures. Original Medicare Parts A and B cover most basic medical services. In general, Medicare Part A covers hospitalizations (i.e., inpatient care) and Medicare Part B covers outpatient care. In addition to inpatient care, Part A also covers home healthcare in limited circumstances, as well as hospice care. Medicare Part B covers outpatient clinical services like doctor’s visits and emergency room visits, including observation. In addition to outpatient care, Part B also covers medical supplies (think splints and casts, or crutches or a wheelchair), X-rays and other radiology services, and preventive care and screening services. One important fact about this last category is that many of the preventive care and screening services covered under Part B are free; there is no coinsurance or other cost-sharing. Screenings for many cancers (including breast, cervical and vaginal, colorectal, and lung) are free, as are screenings for depression and diabetes. Many Medicare beneficiaries do not understand that these screenings, as well as many other preventive services (like flu shots), are free; consequently, they fail to seek out those services. It’s important for you to be aware of and take advantage of these free preventive and screening services to avoid delayed diagnosis and treatment of many different health conditions. Failing to do so can ultimately impact your longevity and quality of life, not to mention increase the eventual cost of treatment when an ailment’s symptoms appear later in a more advanced stage. As the adage goes, an ounce of prevention is worth a pound of cure!

Which Medicare coverage option is right for me?

For the third time in this blog, I must say it again: it depends. Decisions around Medicare are incredibly complex and depend on both medical and financial factors that are individual to each person. Many folks end up talking to their friends or neighbors for advice, but what works best for them may not work best for you! You should do some independent research and consult with your primary care physician or other medical professionals with whom you have an existing relationship so that you can make the most informed choices about the coverage and cost of your healthcare in retirement.

Where can I find out more?

If you want or need to learn more about Medicare, you can utilize other resources from Brianna, Shield Insurance Specialist. We are here to help answer all Medicare coverage questions.

This information is general in nature and is not intended to be tax, legal, accounting, or other professional advice. The information provided is based on current laws, which are subject to change at any time, and has not been endorsed by any government agency.

Nationwide and its representatives do not give legal or tax advice. Please consult an attorney or tax advisor for answers to legal questions.

My Medicare Matters® is a registered trademark of the National Council on Aging.

Nationwide and NCOA are separate and non-affiliated companies.

Nationwide Investment Services Corporation (NISC), member FINRA, Columbus, Ohio. The Nationwide Retirement Institute is a division of NISC.

Cycling has grown significantly in popularity over the past decade. Towns across the country are adding bike lanes to their roads to become more bike-friendly, and more and more people are ditching their cars and using a bike as their primary form of transportation. According to USA Today, larger cities like Portland, Ore., and Minneapolis have more than doubled their rate of bike commuters since 2014 — and as a cyclist, I can’t help but get excited.

Now, with bike riding growing in popularity across the U.S. — it may be a good idea to brush up on some traffic guidelines to avoid any accidents.

When you purchase a bike, you’re likely not required to take a safety class before you ride it. And, for drivers, the instructors touched on bike safety as part of Drivers Ed, but who remembers details from a course they took in their teens?

My point is, adults aren’t given much guidance when it comes to cyclists and cars coexisting on the roads. And as a bicyclist and a driver, I did some research because honestly, I needed a refresher myself.

Safety tips for DRIVERS:

Try to be 3 feet or more away from a bike.

Try to pass on the left when possible.

Blind spots are always lurking, make sure to watch for bikes.

Only pass a bicyclist when your passing lane is free and clear.

Look in your mirror for cyclists when you’re parking.

Always think of cyclists as equals – remember, they have rights on the road too!

Safety tips for BICYCLISTS:

Make sure to ride with the flow of traffic.

Traffic signs and signals aren’t just for cars. Stop on red to be safe.

Use marked bike paths or lanes if they’re available.

Use your arm to make turn signals and take advantage of turn lanes so cars are aware of what you’re doing.

Consider using a mirror to monitor the cars behind you.

If you’re riding at night or in a storm, make sure to use some sort of flashers.

Watch for parked cars.

And most importantly — stay alert at all times.

If you’re unsure about your city’s or state’s traffic laws, it doesn’t hurt to look them up beforehand. No matter what you drive, be sure to enjoy the roads out there safely!

Umbrella insurance is great to have if you want total financial protection. Consumers on the market for umbrella insurance in Michigan can purchase the coverage they’re looking for from Shield Insurance Agency.

It’s essential that you go through a few steps before you purchase an umbrella insurance policy.

The following are three things to do when you’re interested in buying umbrella insurance:

Research umbrella insurance so that you know what you’re getting

Misconceptions about umbrella insurance are common, so it’s important to do your research and make sure you completely understand umbrella insurance before purchasing a policy.

Remember that umbrella insurance protects you against liability expenses. This is not a type of insurance that insures your personal belongings like your vehicle.

Determine what the total value of all your assets is

You’ll need to choose how much coverage to carry when you purchase umbrella insurance. It’s best if you have enough coverage to equal your net worth.

As part of preparing to buy umbrella insurance, it’s good to evaluate your assets and find out what your total net worth is. This will help you to choose the right amount of coverage.

Shop around with different umbrella insurance providers

You’ll have options to pick from when you buy an umbrella insurance policy. You should explore your options so that you can get a policy that meets your specific needs.

Research different umbrella insurance providers in your area and get quotes on policies from numerous companies so that you can compare.

Give Us A Call

Once you’ve done all the things mentioned above, you can choose an umbrella insurance policy that’s right for you. Shield Insurance Agency can come to your assistance to get a quote on an umbrella insurance policy in Michigan.

As we head into the warmer months, it’s a good time to recommit yourself to stay hydrated and happy. As you probably know by now, your body needs to stay hydrated to keep all your organs functioning, your body temperature regulated and to keep your mind running at peak performance. Dehydration is no joke — and can be a surefire way to disrupt your day-to-day life and leave you feeling awful.

“Dehydration is very common, and [it leads] to many symptoms, including fatigue, constipation, and decreased concentration,” Dr. Nancy Rahnama, physician nutrition medical specialist and board-certified internist, tells SheKnows.

Rahnama explains that recommended daily water intake varies depending on many factors, such as a person’s weight, environment, gut function, level of physical activity, and medications they take. But as a general rule, she suggests starting off with 64 ounces (eight cups) of water per day.

We all know that we should diligently be drinking enough water each day, but there’s just one problem: Plain, flat water simply isn’t appealing to a lot of us. Luckily, there are plenty of healthy beverage options that count toward our daily water intake, and drinking them won’t feel like quite as much of a chore.

“Water is considered a liquid beverage without caffeine, alcohol or sugar content,” Rahnama explains.

If you don’t love flat water or you simply want some more variety when you hydrate, try drinking these five beverages. Eight ounces of each is equivalent to eight ounces of regular water and they each contain either zero or very few calories.

Flavored Sparkling Water

If you’d normally reach for a soda to quench your thirst, we have a better (but still fizzy) option for you.

Not only will this give you the flavor-plus-fizz combo you crave from soda, but it’s not full of sugar and empty calories and has the added bonus of some vitamin C from the citrus fruit.

There are also plenty of no-added-sugar flavored seltzer waters to choose from — or for the less adventurous, there’s always plain.

Do you struggle to pinpoint why you’re burnt out at work? Is it you? Is it your job?

It may actually be a mismatch of the two, according to Christina Maslach, a social psychologist, retired professor of psychology at U.C. Berkeley and author of “The Burnout Challenge: Managing People’s Relationships with Their Jobs.”

“You really have to look at the relationship with the job, and that means looking at both the job and the person. It’s not like one or the other,” Maslach tells CNBC Make It.

“It’s certainly not just the person who has to make the changes.”

The cure for burnout isn’t just taking time off or a starting a mindful morning routine, but it’s actually discovering how to get a better match between what your job requires of you and the tools you have to complete your duties, she says.

Maslach, and co-author of her book, Michael P. Leiter, identified six areas within your profession that should meet your standards, or else your risk of more stress and potential burnout increases.

Here are the six factors and how they may be affecting you.

Workload Burnout

It can be extremely difficult to meet high demands when you’re low on resources, says Maslach.

Lacking supportive tools like time, people, equipment or information may be affecting your ability to do your job how you’d like to.

Control

Having autonomy, discretion and an ability to make choices are necessary in the workplace in order to feel like you’re doing your job well, she notes.

“People often complain about having a lack of control, that they’re told what to do, no ifs, ands or buts about it,” she says.

Reward

The way you feel about your salary and benefits can influence your emotions toward work. But, rewards aren’t just limited to finances.

“A lot of times, it’s social recognition, that people are pleased by what you’ve done and let you know it,” Maslach says. If you’re working hard and aren’t receiving positive feedback, you’re more likely to feel unjustified.

Community Burnout

From co-workers, bosses, and people you supervise to clients, patients, or students, everyone you interact with while working can affect your feelings about your job. Without mutual respect, trust, and support within your team, even the best job can turn into a “socially toxic workplace” that you hate, says Maslach.

Fairness

“Where there’s an absence of fairness, this is where discrimination lives. This is where glass ceilings exist,” Maslach says.

Rules, policies and practices should feel equal in your work environment or it can lead to resentment, she adds. You need to believe that you have an equal chance at receiving promotions and just as many opportunities as the rest of your team.

Values

You’re a lot more likely to quit your job if it doesn’t align with your basic moral principles, says Maslach.

Working for a company or organization where there are ethical conflicts can deter you from feeling enthusiastic about what you do, she notes.